Homeownership is Calling: Why the September Market Report is Great News for VA and FHA Buyers

The housing market is showing encouraging signs as we head toward the end of the year, making it an excellent time for aspiring homeowners, especially those utilizing VA or FHA loans.

A recent analysis of the National Association of Realtors® (NAR) Existing-Home Sales Report for September 2025, as highlighted on Realtor.com, points to a market shift that directly benefits first-time and low-down-payment buyers.

Here is a breakdown of the key market opportunities and how your VA or FHA benefits, backed by Loan Goal’s flexible underwriting, can help you achieve your #LoanGoal.

The September Market Shift: Sales Up, Affordability Improving

The NAR data confirms that conditions are aligning to favor buyers:

- Sales are Rising: Existing-home sales saw an increase of 1.5% month-over-month. According to NAR Chief Economist Lawrence Yun, this increase is thanks to falling mortgage rates that are “lifting home sales” and improving affordability.

- Prices Remain Stable: The median existing-home price of $415,200 was up only 2.1% year-over-year. This modest, slow-down pace of price appreciation indicates a less volatile market than in previous years.

- Inventory is Up: Total housing inventory is up 14.0% from September of last year, giving you more choices and reducing the pressure of bidding wars.

- First-Time Buyers are Back: Most importantly, at least 30% of sales in September were made by first-time homebuyers. This significant increase from the previous year shows that market entry is becoming more accessible.

Realtor.com’s Chief Economist Danielle Hale noted that with falling rates and lower competition during the autumn months, buyers can count on an edge to potentially secure lower prices—especially in the lower price tiers. This is your window of opportunity.

Your Key to Entry: Flexible VA and FHA Loans

The current market conditions—improving affordability, more inventory, and a higher share of first-time buyers—are perfectly suited for government-backed loans. VA and FHA loans are designed specifically to overcome common barriers to homeownership, such as large down payments and stringent credit requirements.

At Loan Goal, we specialize in maximizing these programs with our flexible lending guidelines.

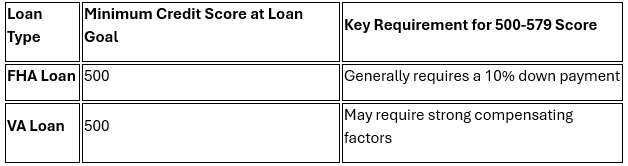

We Go Down to a 500 Credit Score

While many lenders have rigid credit minimums, Loan Goal offers programs that can help borrowers with lower credit scores:

The Power of Manual Underwriting for VA and FHA Clients

The automated systems most lenders use often reject applications based solely on a lower credit score. This is where Loan Goal truly separates itself. We offer manual underwriting when needed.

What is Manual Underwriting?

Instead of a computer giving an automatic yes or no, a skilled underwriter personally reviews your entire financial profile. This allows us to consider compensating factors that an automated system ignores, such as:

- Verified History of On-Time Rent Payments: Showing you can responsibly handle a housing expense.

- Low Debt-to-Income (DTI) Ratio: Demonstrating you have significant income left after paying off debt.

- Substantial Cash Reserves: Having savings to cover a few months of payments in an emergency.

This detailed, human review is crucial for buyers who have the income and stability to own a home but whose credit score is below the typical 620-640 cutoff. For our VA and FHA clients, manual underwriting can be the bridge to homeownership.

Ready to Act? Your Next Step

Loan Goal is proud to serve borrowers across the country. Our commitment to flexible VA and FHA underwriting applies no matter where you are looking to purchase.

The September report confirms that momentum is shifting in favor of the buyer. With falling rates and higher inventory creating a more favorable environment, now is the perfect time to leverage the power of VA or FHA financing with a lender who is committed to getting you approved.

Don’t let a past credit issue stop you from achieving your homeownership goals. Call Loan Goal today to discuss your VA or FHA eligibility—even with a 500 credit score—and see if manual underwriting is right for you.